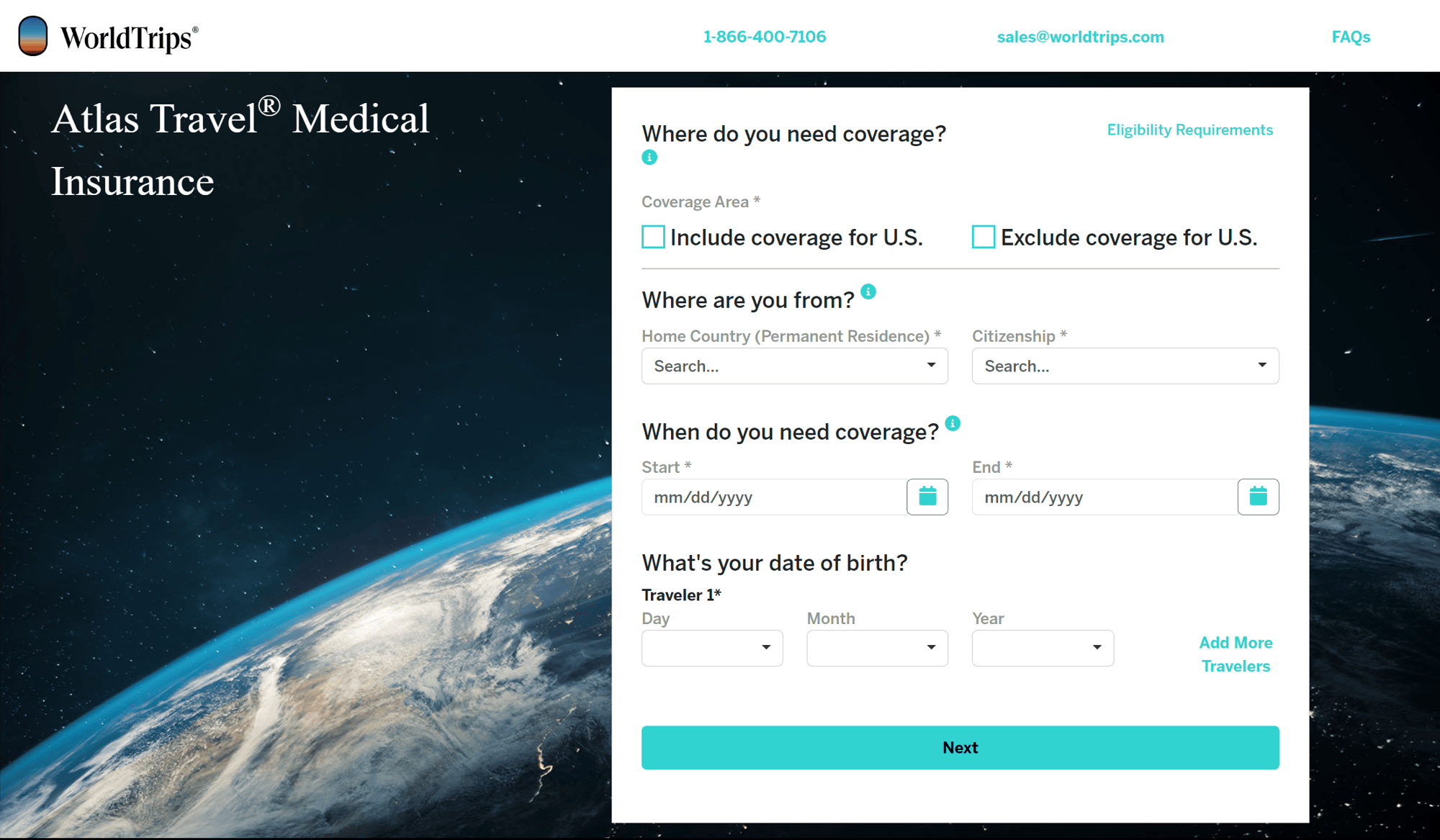

You’ll need to begin by answering the question of whether your coverage includes the U.S. or excludes the U.S. Select the box that best describes your trip’s coverage area.

- If your destination includes the 50 U.S. states, Puerto Rico, and/or U.S. Virgin Islands -> check “Include coverage for U.S..”

- If your destination includes Guam, American Samoa, Northern Mariana Islands, and/or no other part of the U.S. -> check “Exclude coverage for U.S.”

But, what about layovers within the U.S.?

- If you are a U.S. citizen or resident and your trip includes a layover within the 50 U.S. states, Puerto Rico, and/or U.S. Virgin Islands prior to your departure from the U.S. -> check “Exclude coverage for U.S.”

- If you’re a non-U.S. citizen or non-U.S. resident and your trip includes a layover within the 50 U.S. states, Puerto Rico, and/or U.S. Virgin Islands -> check “Include coverage for U.S.” if you want coverage during your layover

Note: Click the “Eligibility Requirements” link at the top right of the quote engine for details regarding plan eligibility.

If you select “Include coverage for U.S.,” a “Destination(s)” section with appear and the United States will automatically be added. Where it says “Search” type in any additional destinations or click the drop-down arrow and select your trip destination(s). Include ALL destinations for which you would like to be covered. Click the teal “x” to the right of the destination to remove it.

Then, under “Primary U.S. Destination” select the state in which you will spend the most time. If you are spending equal time in multiple U.S. states, choose the state you will visit first.

If you select “Exclude coverage for U.S.,” a “Destination(s)” section will appear. Either type in your destination(s) in the search bar or use the drop-down arrow to add the destination(s) to which you are traveling. Include ALL destinations for which you need coverage. Click the teal “x” to the right of the destination to remove it from the list.

NOTE: Certain countries are currently excluded from coverage due to U.S. government sanctions. If you’re not sure whether your destination is excluded, contact WorldTrips at (877) 690-9859. Additionally, certain benefits, such as the Political Evacuation and Terrorism benefits, are restricted based on U.S. Department of State and the Centers for Disease Control and Prevention (CDC) travel advisories, as indicated in the policy wording. Review the Atlas Travel policy wording and the complete list of travel warnings by the U.S. Department of State.